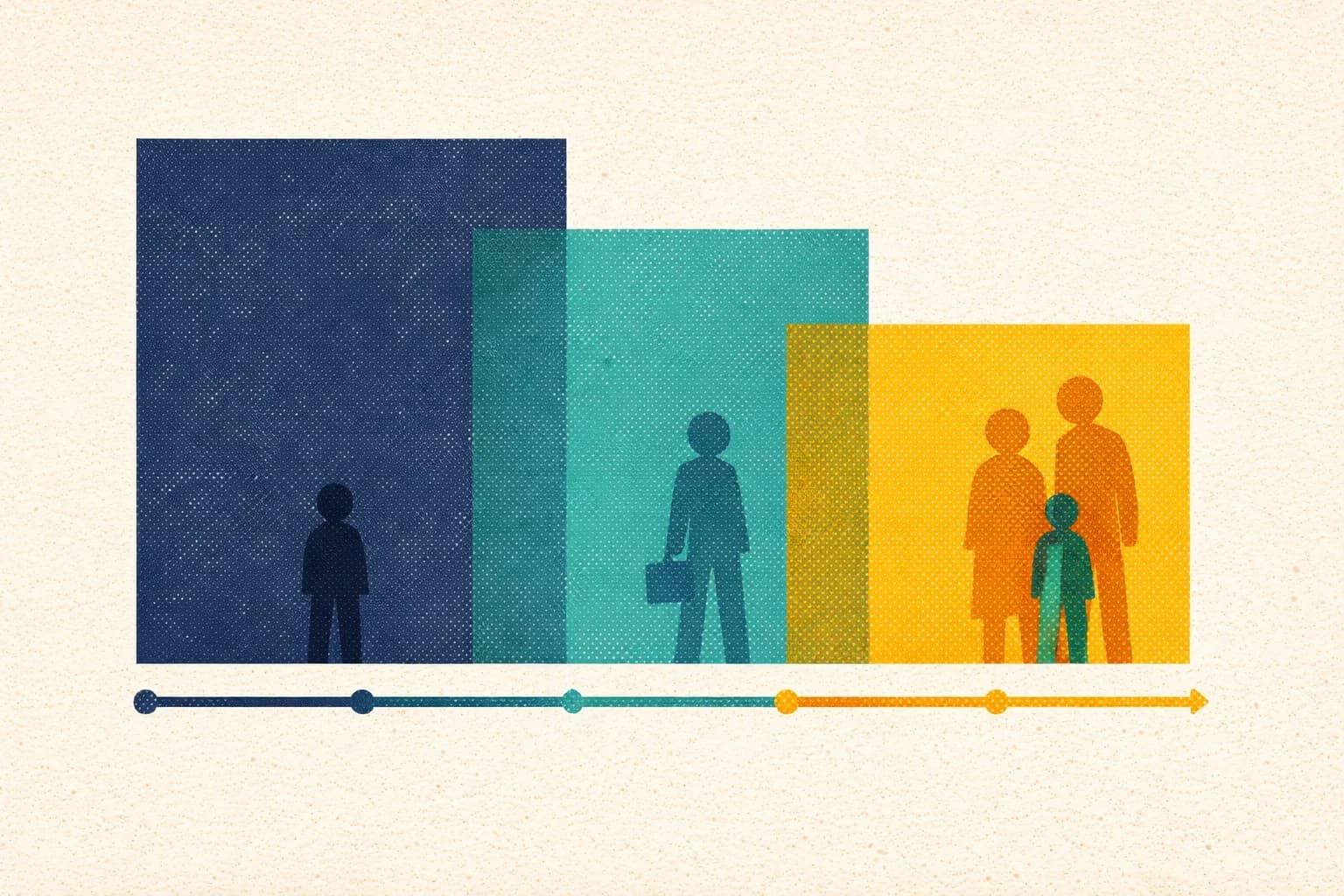

The standard approach to term insurance in India is simple: buy one large policy that covers all your financial obligations. A ₹1 crore or ₹2 crore policy, purchased in your late 20s or early 30s, and held until retirement. It works, but it is not the only approach, and it may not be the most efficient one.

Staggered term insurance means buying multiple smaller policies at different life stages instead of one big policy. Each policy is sized to match the specific financial obligation it is meant to cover. As obligations are met (loan paid off, children become independent), you let the corresponding policy lapse. The result: your total premium bill decreases over time, matching your decreasing need for coverage.

Cheat Sheet

•

Staggered insurance: Buy 2-3 smaller policies at different life stages instead of one large policy.

•

Key advantage: You can drop policies as obligations are met, reducing total premiums over time.

•

Insurer diversification: Multiple policies from different insurers reduce the risk of a single insurer delaying or disputing your claim.

•

Slight premium premium: Total premiums for staggered policies may be 5-15% higher than a single equivalent policy, but the flexibility to drop policies saves money over the full term.

•

Best for: People whose financial obligations will clearly decrease over time (loan repayment, children aging out of dependence).

How Staggered Insurance Works

Instead of buying one ₹2 crore policy at age 30, you might structure it like this:

| Policy | Purpose | Cover | Term | Drop When |

|---|---|---|---|---|

| Policy A (age 30) | Income replacement for family | ₹1 crore | 25 years (to age 55) | When children are independent + retirement corpus built |

| Policy B (age 32) | Home loan coverage | ₹50 lakh | 20 years (matching loan tenure) | When home loan is fully repaid |

| Policy C (age 35) | Children’s education fund | ₹50 lakh | 15 years (until children finish college) | When education costs are funded |

Total cover at age 35: ₹2 crore (same as a single policy). But by age 47, the home loan is paid off, and Policy B lapses. By age 50, children are through college, and Policy C lapses. From age 50 to 55, only Policy A remains active, at a much lower premium than the original ₹2 crore single policy would have been.

Staggered vs Single Policy: A Cost Comparison

Let us compare the two approaches for a 30-year-old healthy non-smoking male:

| Approach | Annual Premium (approximate) | Total Premiums Paid Over Full Term |

|---|---|---|

| Single ₹2 crore policy, 25-year term | ₹16,000/year for 25 years | ₹4,00,000 |

| Staggered: ₹1 Cr (25yr) + ₹50L (20yr) + ₹50L (15yr) | ₹8,500 + ₹4,200 + ₹4,800 = ₹17,500/year initially | ₹3,72,500 (because two policies end early) |

Note: These are approximate figures. Actual premiums depend on the insurer, health profile, and policy terms.

The staggered approach costs slightly more per year initially (₹17,500 vs ₹16,000), but the total premiums paid over the lifetime are lower because two policies end before the 25-year mark. The savings compound in the later years when you are no longer paying for coverage you do not need.

Did You Know

Staggered policies often cost more upfront but less in total — because you stop paying premiums for coverage you no longer need, not because the individual policy rates are lower.

“Coverage should increase with responsibilities: moderate increase at marriage, significant increase with the first child, and reassessment with a second child. As children become financially independent, gradual reduction is possible. Near retirement, coverage may reduce if there are sufficient assets.”

— Sneha Wani, Chartered Accountant, Mumbai

Five Advantages of Staggered Insurance

1. Coverage tracks your actual needs

Your financial obligations peak in your mid-30s to mid-40s (home loan + children + aging parents) and decline as debts are paid off and children become independent. A single large policy covers you at the same level throughout, even when your need has halved. Staggered policies let your coverage naturally decrease as obligations reduce.

2. Insurer diversification

Holding policies with 2-3 different insurers reduces concentration risk. If one insurer delays a claim (due to investigation, documentation disputes, or processing backlogs), the other policy can still pay out promptly. This is particularly important for large coverage amounts where a single claim delay could leave your family without funds for months.

Industry claims repudiated by amount: how much nominees lost each year

FY 2020-21

₹925 cr

FY 2021-22

₹1,292 cr

FY 2022-23

₹1,050 cr

FY 2023-24

₹893 cr

FY 2024-25

₹976 cr

Source: IRDAI Annual Reports, 2020-21 to 2024-25

3. Flexibility to adjust

With a single policy, your only options are to keep it or surrender it (losing all premiums paid). With multiple policies, you can selectively drop the ones that are no longer needed while keeping the others active. This is far more flexible than trying to reduce the sum assured on a single policy (which most insurers do not allow).

4. Nominee flexibility

Different policies can have different nominees. Policy A (income replacement) could name your spouse. Policy B (home loan) could be assigned to the lender. Policy C (children’s education) could name a trust or specific family member. With a single policy, you have one nominee for the entire amount, which requires your family to manage the distribution themselves.

Did You Know

Each policy in a staggered setup can have a separate nominee — you can direct the home loan policy payout to your lender, the income replacement policy to your spouse, and the education fund policy to a guardian for your child.

5. Lower total lifetime premiums

Because shorter-term policies have lower per-year premiums and because you stop paying for dropped policies, the total premiums paid over your lifetime are often lower than a single large policy held to full term. The exact savings depend on when you drop each policy.

When Staggered Insurance Does NOT Make Sense

- Your financial obligations are stable: If you expect to support dependents at the same level for your entire working life (e.g., lifelong support for a dependent with special needs), a single large policy with a long term is simpler.

- You value simplicity: Managing 2-3 policies means 2-3 premium payment dates, 2-3 renewal reminders, and more paperwork for your nominee at claim time. If you prefer simplicity, one policy is easier.

- Health may deteriorate: If you have health conditions that could worsen, buying all your coverage now (while you are healthy) at standard rates may be better than buying additional policies later when you might face loading or rejection.

Case Study: The Sharma Family’s Approach

Rahul Sharma, 31, earns ₹18 lakh/year. He has a new home loan (₹55 lakh, 20-year tenure), a 1-year-old daughter, and his wife Meena works part-time earning ₹4 lakh/year. His total coverage need: ₹1.8 crore (income replacement) + ₹55 lakh (home loan) + ₹40 lakh (daughter’s education) = ₹2.75 crore.

Instead of one ₹3 crore policy for 25 years, Rahul buys:

- Policy A: ₹1.5 crore, 25-year term (income replacement) with Insurer X. Annual premium: ₹12,500.

- Policy B: ₹60 lakh, 20-year term (home loan cover, assigned to lender) with Insurer Y. Annual premium: ₹4,200.

- Policy C: ₹50 lakh, 18-year term (daughter’s education fund) with Insurer X. Annual premium: ₹3,800.

Total cover: ₹2.6 crore. Total annual premium: ₹20,500.

At age 49, the daughter finishes college. Rahul drops Policy C, saving ₹3,800/year. At age 51, the home loan is paid off. He drops Policy B, saving ₹4,200/year. From age 51-56, only Policy A remains active at ₹12,500/year. Total premiums paid over 25 years: approximately ₹4.5 lakh (compared to ~₹5.2 lakh for a single ₹3 crore policy held for the full term).

17,333

Individual death claims repudiated across the industry in FY 2024-25, with another 4,999 still pending at year-end. When your family holds policies with two or three different insurers, a dispute with one does not freeze the entire payout.

IRDAI DATASource: IRDAI Annual Report 2024-25

FAQs

Is it better to buy one large policy or multiple smaller ones?

If your financial obligations will decrease over time (which is true for most people), staggered policies offer better flexibility and often lower total lifetime premiums. If your obligations are constant or you prefer simplicity, a single policy works fine.

Can I buy policies from different insurers?

Yes, and this is actually one of the benefits of staggering. It diversifies your insurer risk. When applying, you must disclose existing policies to each insurer. Your total cover across all policies should be proportional to your income (most insurers cap total coverage at 15-20x annual income).

Key Fact

Most insurers cap total life insurance cover at 15–20 times your annual income, across all policies combined. This limit applies whether you hold your policies with one insurer or spread them across several.

How do I manage premium payments for multiple policies?

Set up auto-debit for each policy. Keep a simple spreadsheet or note with policy numbers, insurer names, premium amounts, due dates, and nominee details. Share this information with your spouse or nominee so they know which policies exist and how to claim.

What if I cannot get a new policy later due to health issues?

This is a valid concern. If you have a family history of health conditions or are worried about future insurability, buy all the coverage you need now while you are healthy. You can still structure it as multiple policies purchased at the same time with different terms, giving you the staggered benefit without the health risk of delayed purchases.

Watch Out

If your health worsens between policy purchases, a later insurer may load your premium significantly or reject your application outright. Build in your full coverage need early, while standard rates still apply to you.

Does staggering increase my total claim amount if I die?

No. The total death benefit is the sum of all active policies. If all three policies are active, your nominee gets the combined amount. If you have dropped some policies, the payout is only from the remaining active ones. The total claim is the same as (or less than) a single policy of equivalent value.

Is Staggered Insurance Right for You?

Staggered term insurance is not for everyone, but it is a smarter approach for people whose financial obligations clearly decrease over time. By matching each policy to a specific obligation and dropping it when that obligation is met, you pay only for the coverage you need, when you need it. The result is more flexibility, insurer diversification, and often lower total lifetime premiums compared to a single large policy. If your financial life is getting simpler as you age (loans paid off, children independent, retirement savings growing), staggered insurance deserves a serious look.

Related Reading

Try our free tools

Disclaimer: This article is for informational purposes only and does not constitute insurance advice. Consult an IRDAI-registered insurance advisor for recommendations tailored to your specific financial situation and needs.

Was this article helpful?

Your feedback helps us improve our guides

Expert contributor

SW

Sneha Wani

Chartered Accountant, Mumbai

Reviewed and Edited by

Hardik LashkariHardik Lashkari is a Chartered Accountant and finance content specialist with over six years of experience writing for fintech and financial services brands. He specialises in translating complex financial topics into clear, credible content — from insurance and taxation to investing and personal finance. At Gyansurance, Hardik covers the how-to side of term insurance: buying guides, policy maintenance, digital underwriting, and the fine print buyers often miss.