Imagine being 30 today with a young family, a home loan, and financial responsibilities. You consider term insurance: coverage till 65 or “till 99.” While lifelong coverage sounds reassuring, it comes at a high cost. This article explores why, for many Indian policyholders, coverage till about age 65 is often more cost-efficient, practical, and suited to real financial needs.

TL;DR

- Premiums for coverage till 99 are often 50–100% higher than till 65.

- Most major liabilities end around retirement: home loans, children’s education, dependency.

- Inflation erodes real value of late-life payouts.

- Health risks, underwriting, and limited product choices make long-term coverage expensive.

- Matching coverage to financial life cycles offers better cost-benefit efficiency.

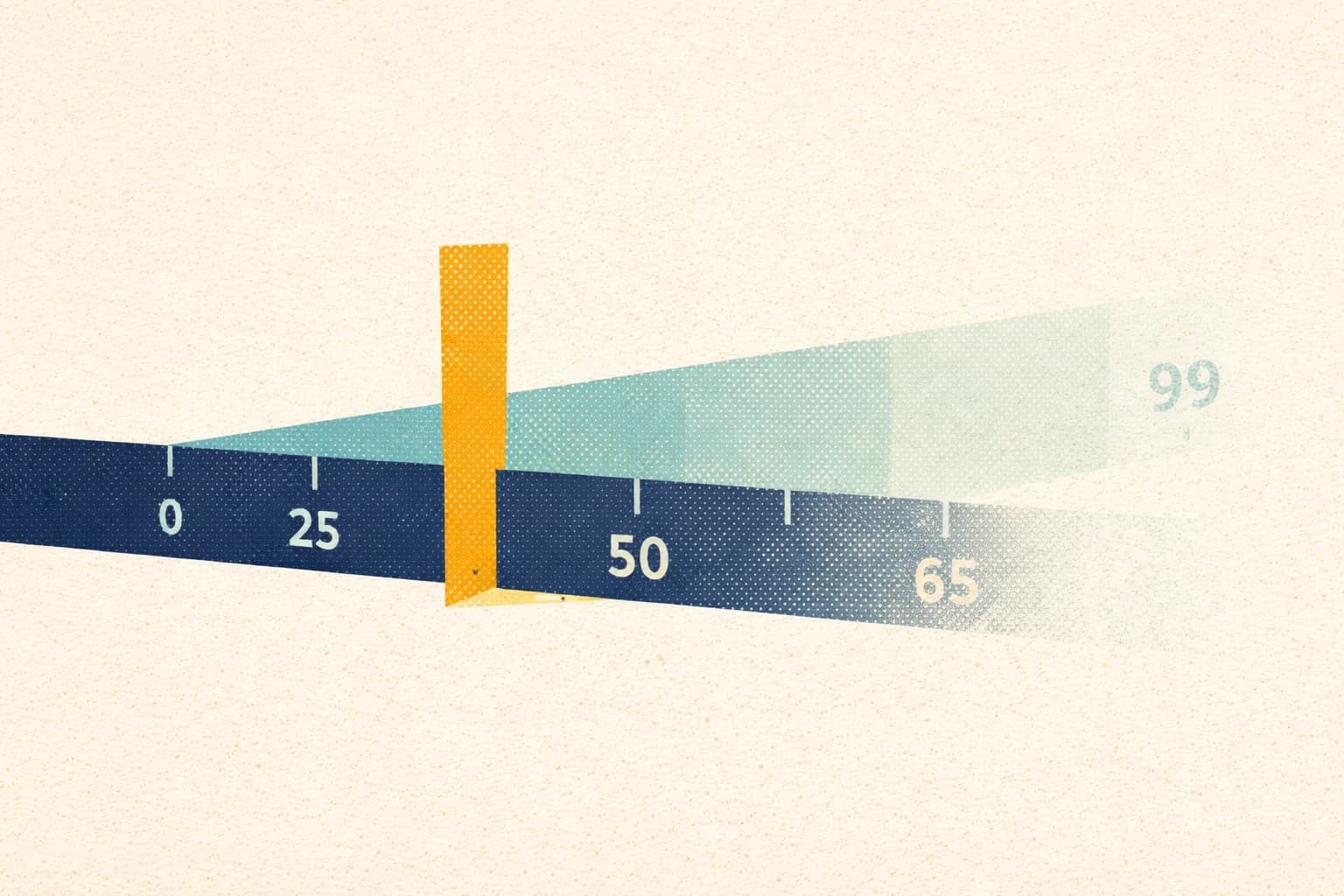

Coverage Till 65 vs Till 99

Coverage till 65 ends at retirement or liability completion; surviving beyond 65 provides no benefit. Coverage till 99 (or whole-life term) ensures death benefit anytime, even in late life, but comes with higher premiums, stricter underwriting, and potential diminishing returns due to inflation.

Cost Differences

Premium Escalation: For a healthy 30-year-old male seeking ₹1 crore cover, ICICI Prudential shows premiums rising from ₹12,683 (till 60) to ₹34,015 (till 99): a 168% increase. Extending from 60 to 70 increases ~30–70%, depending on the insurer.

Watch Out

For a 30-year-old buying ₹1 crore cover, the annual premium can jump 168% — from ₹12,683 to ₹34,015 — simply by extending coverage from till-60 to till-99.

Lifetime Premium vs Benefit: Most financial liabilities: children, home loans, debt: peak before 65. Paying high premiums for coverage after retirement often provides little incremental value.

Matching Coverage to Your Financial Life Cycle

Peak Liabilities: Ages 25–60 involve highest obligations: children, mortgages, supporting parents. Coverage beyond 65 offers diminishing marginal benefit.

Retirement Changes: Post-retirement income usually drops; high premiums can strain cash flow. Insurers require stricter underwriting at older ages, pushing premiums higher.

Mortality, Probability & Value

98.32%

Industry claim settlement ratio (by count)

FY 2024-25

—Stable at ~98% since FY 2017-18

₹33,697 cr

Total individual death claims paid

FY 2024-25

▲+17% from ₹28,868 cr in FY 2023-24

Mortality Risk: Death probability rises sharply after 70; premiums for late-life coverage are disproportionately high.

Inflation Impact: A payout at age 99 will have far less real value. Even ₹1 crore decades later may not cover intended expenses unless coverage is significantly higher, further escalating premiums.

Did You Know

A ₹1 crore payout decades from now buys far less than ₹1 crore does today — to maintain real value, you’d need significantly higher cover, which makes till-99 premiums even steeper.

Practical Considerations

Availability & Underwriting: Policies till 99 are fewer, more expensive, with stricter health requirements and exclusions.

₹

976 cr

Total value of repudiated individual death claims across the industry in FY 2024-25. Stricter underwriting on longer-tenure policies increases rejection risk.

IRDAI DATASource: IRDAI Annual Report 2024-25

Opportunity Cost: Extra premium for long coverage could be invested elsewhere to better serve dependents’ needs.

Quick Tip

Put the premium difference between a till-65 and a till-99 policy into a PPF or equity fund. Your dependents get a growing asset they can access any time, not just on your death.

Emotional Comfort: “Till 99” offers peace of mind but can lead to over-insurance, reducing financial flexibility.

Example: ₹1 Crore Cover (Male, Age 30)

| Coverage End Age | Annual Premium | % Increase vs Till 60 |

|---|---|---|

| 60 | ₹12,683 | Reference |

| 65 | ₹14,343 | 13% |

| 70 | ₹15,303 | 21% |

| 99 | ₹34,015 | 168% |

When “Till 99” Makes Sense

- Lifelong dependents (e.g., special needs child)

- Desire for a legacy

- Expecting serious late-life health risks

- Low-confidence investment environment

Even then, cost-benefit analysis is essential.

Fictional Example

Ravi, 35, married with two children, has a home loan.

- Till 65: Pays ₹15,000/year; major obligations end by 60; remaining funds can support retirement savings.

- Till 99: Premium doubles to ₹33,000/year; late-life benefit is eroded by inflation; less financial flexibility.

FAQs

Will “till 99” help if I live past 80?

Yes, but consider dependents’ needs, inflation, and opportunity cost of higher premiums.

Are claims harder for policies till 99?

Often yes: stricter underwriting, waiting periods, exclusions apply.

How does taxation differ?

Both offer similar tax benefits; higher premiums for longer coverage provide larger absolute deductions.

Can I extend coverage later?

Conversion is possible but costly, with stricter health checks.

How to choose the right term?

Match coverage to liabilities, add a buffer, and compare premiums vs investment opportunities.

Trade-Off Table

| Factor | Till 65 | Till 99 / whole life |

|---|---|---|

| Premium Cost | Relatively low | Much higher |

| Financial Liabilities | Covers peak obligations | Extends into retirement |

| Flexibility / Cash Flow | Better | Lower |

| Inflation Impact | Moderate | High |

| Opportunity Cost | Can invest saved premiums | More funds locked |

| Emotional / Legacy Benefit | Limited beyond 65 | Lifetime coverage, legacy |

Matching Coverage to Need

For most Indian earners, coverage till 60–65 protects during peak financial responsibility, costs less, and allows flexibility for retirement and emergencies. “Till 99” may appeal for legacy or lifelong dependents, but usually represents paying far higher premiums for benefits of limited practical value. Matching insurance to liabilities, income cycles, and real needs ensures smarter, cost-effective coverage.

Related Reading

Try our free tools

Disclaimer: This article is for informational purposes only and does not constitute insurance advice. Consult an IRDAI-registered insurance advisor for recommendations tailored to your specific financial situation and needs.

Was this article helpful?

Your feedback helps us improve our guides

Reviewed and Edited by

Hardik LashkariHardik Lashkari is a Chartered Accountant and finance content specialist with over six years of experience writing for fintech and financial services brands. He specialises in translating complex financial topics into clear, credible content — from insurance and taxation to investing and personal finance. At Gyansurance, Hardik covers the how-to side of term insurance: buying guides, policy maintenance, digital underwriting, and the fine print buyers often miss.