The 3-year clock: when it starts, when it resets, and what resets it

Updated 11 min read

swipe to read →

Section 45(1) says the contestability period runs from the date of issuance, commencement of risk, revival, or rider addition. “Whichever is later” means the most recent event controls.

swipe to read →

If your policy lapses and you revive it, the 3-year contestability period starts fresh. A policy that was 2.5 years old goes back to day one on revival. The 2015 amendment explicitly added “revival” as a trigger date.

swipe to read →

Adding a critical illness or accidental death rider starts a separate 3-year period for that rider. Your base policy’s clock is unaffected. You can have a protected base policy with a still-contestable rider.

swipe to read →

Premium payments, nominee changes, address updates, policy assignments, and premium frequency changes have no effect on the contestability period. Only revival and rider addition reset the clock.

swipe to read →

The simplest way to protect your family is to never let the clock reset. Set up auto-debit. Treat lapsing as a last resort.

swipe to continue →

Everyone knows the “3-year rule” under Section 45 of the Insurance Act. After 3 years, your insurer cannot question your policy on any ground whatsoever. What most people miss is when that 3-year period actually begins and what can reset it to zero.

This matters because a policy that you think is “safe” (past 3 years) may not be if you let it lapse and revived it, or if you added a rider recently. Your family’s claim depends on knowing where the clock actually stands.

Section 45(1) of the Insurance Act (as amended in 2015) specifies four possible start dates for the contestability period:

The statute says “whichever is later.” This means the 3-year clock runs from the most recent of these four events. For a straightforward new policy with no riders and no lapse, the start date is typically the date of issuance or commencement of risk (often the same day, or within days of each other).

Here is what happens when a policy lapses and is revived:

| Event | Date | Contestability clock |

|---|---|---|

| Policy issued | January 2020 | Starts: January 2020 |

| Premiums paid on time | 2020-2022 | Running (2+ years elapsed) |

| Premium missed, policy lapses | March 2022 | Paused (2 years, 2 months elapsed) |

| Policy revived | September 2023 | Restarts: September 2023 (back to zero) |

| 3-year protection reached | September 2026 | Section 45(1) protection begins |

Without the lapse, this policyholder would have had Section 45(1) protection from January 2023. Because of the lapse and revival, protection is delayed to September 2026. That is 3 years and 8 months of additional exposure.

If you miss premium payments and your policy lapses, then later revive it (either within the revival window or through reinstatement), the 3-year contestability period starts fresh from the revival date. This is explicit in the amended Section 45(1), which lists “the date of revival of the policy” as one of the trigger dates.

This is a significant change from the old law. Under the pre-2015 Section 45, courts held that revival did not restart the clock. The Supreme Court in Reliance Life vs Rekhaben Rathod (2019, decided under the old law) treated the original policy date as the reference point. The 2015 amendment explicitly overrode this by adding “revival” to the list of trigger dates.

Under the old Section 45, courts held that revival did NOT restart the contestability clock. The 2015 amendment explicitly changed this. If you revive a lapsed policy today, your 3-year protection starts over from the revival date.

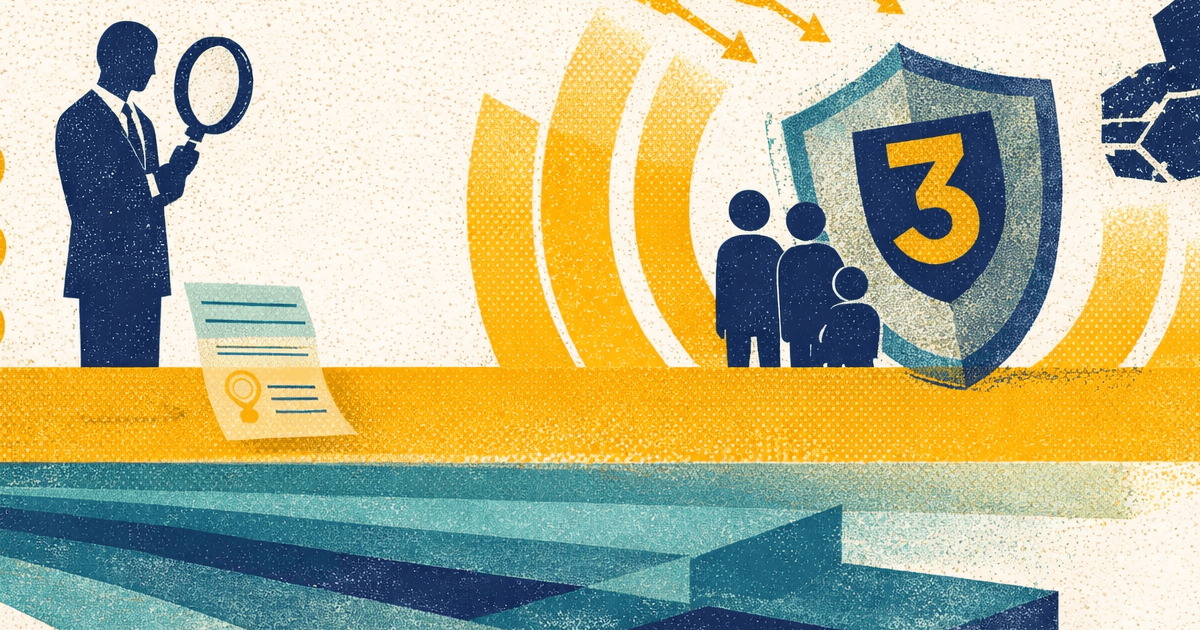

Adding a new rider (such as critical illness, accidental death benefit, or waiver of premium) triggers a fresh 3-year clock for that rider. Section 45(1) lists “the date of the rider to the policy” as a trigger date.

An important distinction: the rider clock is separate from the base policy clock. If your base term insurance policy was issued in 2020 and you add a critical illness rider in 2024, the base policy has already crossed the 3-year mark and is protected under Section 45(1). The rider, however, will only be protected from 2027 onwards. If the insurer investigates a claim related to the rider within those 3 years, the rider can be contested even though the base policy cannot.

Some insurers require a fresh medical examination when reinstating a lapsed policy, effectively treating it as a new underwriting event. In such cases, the contestability clock runs from the reinstatement date, just as it does with revival. The legal basis is the same: Section 45(1) lists revival as a trigger date, and reinstatement with fresh underwriting is functionally equivalent to revival.

Not every change to your policy resets the contestability period. These routine events leave the original clock intact:

The practical cost of a lapse goes beyond late fees and reinstatement charges. When your policy lapses and you revive it, you lose your accumulated contestability protection. A policy that was 2 years and 11 months old and one month away from the 3-year safe zone goes back to zero on revival.

This means the insurer regains full investigation rights for the next 3 years. If the policyholder dies during this new contestability window, the insurer can examine the original proposal form, request medical records, check the IIB (Insurance Information Bureau) database, and potentially repudiate the claim for non-disclosure or misrepresentation.

A common trap: you miss premiums for 6 months, revive the policy, and assume you are still protected because the original policy is “old.” You are not. The clock restarted. Your family is back in the investigation window. Set up auto-debit for premium payments and treat lapsing as a last resort, not an inconvenience.

Revival comes at a cost. Most insurers charge a revival fee and may require a fresh medical examination. If your health has deteriorated since the original policy, the insurer could decline to revive it altogether, or revive it with exclusions or a premium loading. You would then need to buy a new policy at your current age and health status, which will almost certainly be more expensive.

What this means for you

Pay your premiums on time. Set up auto-debit. If your policy does lapse, revive it as soon as possible, but understand that the 3-year contestability clock starts fresh from the revival date. If you are adding a rider to an existing policy, know that the rider faces its own 3-year window even if the base policy is already protected. The simplest way to stay protected is to never let the clock reset in the first place.

Yes. The amended Section 45(1) explicitly lists “the date of revival of the policy” as a trigger date, with “whichever is later” applying. When you revive a lapsed policy, the 3-year contestability period starts fresh from the revival date, regardless of how long the original policy was in force before lapsing.

No. Adding a rider restarts the clock only for that specific rider. Your base policy retains its original contestability timeline. If your base policy was issued in 2020 and is past the 3-year mark, it remains protected under Section 45(1) even if you add a new rider in 2025. The rider itself, however, faces a fresh 3-year contestability period starting from 2025.

Missing one payment does not immediately restart the contestability clock. Most policies have a grace period (30 days for annual/semi-annual premiums, 15 days for monthly). If you pay within the grace period, the policy continues as if nothing happened. If you miss the grace period, the policy lapses. You would need to apply for revival, and that revival restarts the 3-year clock.

No. Changing the premium payment frequency is an administrative change that does not affect the contestability period. The 3-year clock continues running from the original start date (or the most recent revival/rider date, whichever is later).

Your base term insurance policy is protected under Section 45(1) because it has crossed the 3-year mark. The critical illness rider, however, is still within its own contestability period (1 year old, with 2 years remaining). If the insurer investigates a claim related to the rider, the rider can be contested. The base death benefit cannot. These are separate clocks running in parallel.

This article draws on three sources. First, the statutory text of Section 45 of the Insurance Act, 1938, as amended by the Insurance Laws (Amendment) Act, 2015 (Act 5 of 2015, effective 23 March 2015). All statutory quotes are taken directly from the Act; none are paraphrased.

Second, a Gyansurance AI-assisted analysis of 994 court cases involving life insurance claim disputes across the Supreme Court, NCDRC, State Consumer Dispute Redressal Commissions, and High Courts. Cases were sourced from publicly available judgments on the National Judicial Data Grid, the NCDRC website, and Indian Kanoon. Each case was classified by the legal issue raised, the court’s reasoning, the outcome, and whether the old (pre-2015) or amended Section 45 applied. Win rates and patterns reported in this article are derived from this dataset.

Third, the Law Commission of India’s Report No. 190 (2003), which recommended the restructuring of Section 45 and informed the 2015 amendment.

On the fraud question, we present both the statutory argument (which favours policyholders) and the contract law argument (which favours insurers) with the supporting evidence for each. The Supreme Court has not ruled on whether “on any ground whatsoever” in the amended Section 45(1) bars fraud-based challenges after 3 years. Until it does, we do not treat either position as settled law. Where we note that the weight of evidence favours one side, we explain why.

Disclaimer: This article is for informational purposes only and does not constitute insurance advice. Consult an IRDAI-registered insurance advisor for recommendations tailored to your specific financial situation and needs.

Was this article helpful?

Your feedback helps us improve our guides

Reviewed and Edited by

Ashok HegdeAshok Hegde is the Chief Executive Officer at Quantent, where he leads a team of media professionals helping clients leverage digital media for better business outcomes. With over 30 years of experience across print and digital media, he advises clients on content and media strategy — from startups to established brands. His focus is on helping organisations use online media — social, search, and mobile — to build brand awareness, drive sales, and protect reputation.

Who proves fraud when an insurer rejects your claim? Section 45 puts the burden on the insurer — but only for fraud. Know the legal test, the 3-year limit, and how courts actually decide.

Section 45 of the Insurance Act 1938 sets a 3-year limit on contesting life insurance policies. But fraud changes everything. Exact timelines, exceptions, and what courts have ruled.

Your family buys term insurance expecting that if the worst happens, the claim will be paid without hassle. In most cases, it is. Industry-wide claim settlement ratios in India are above 98%. But the remaining 1-2% of claims that get delayed, disputed, or denied are often caused by issues that were completely preventable. These are … Read more