Cheat Sheet

•

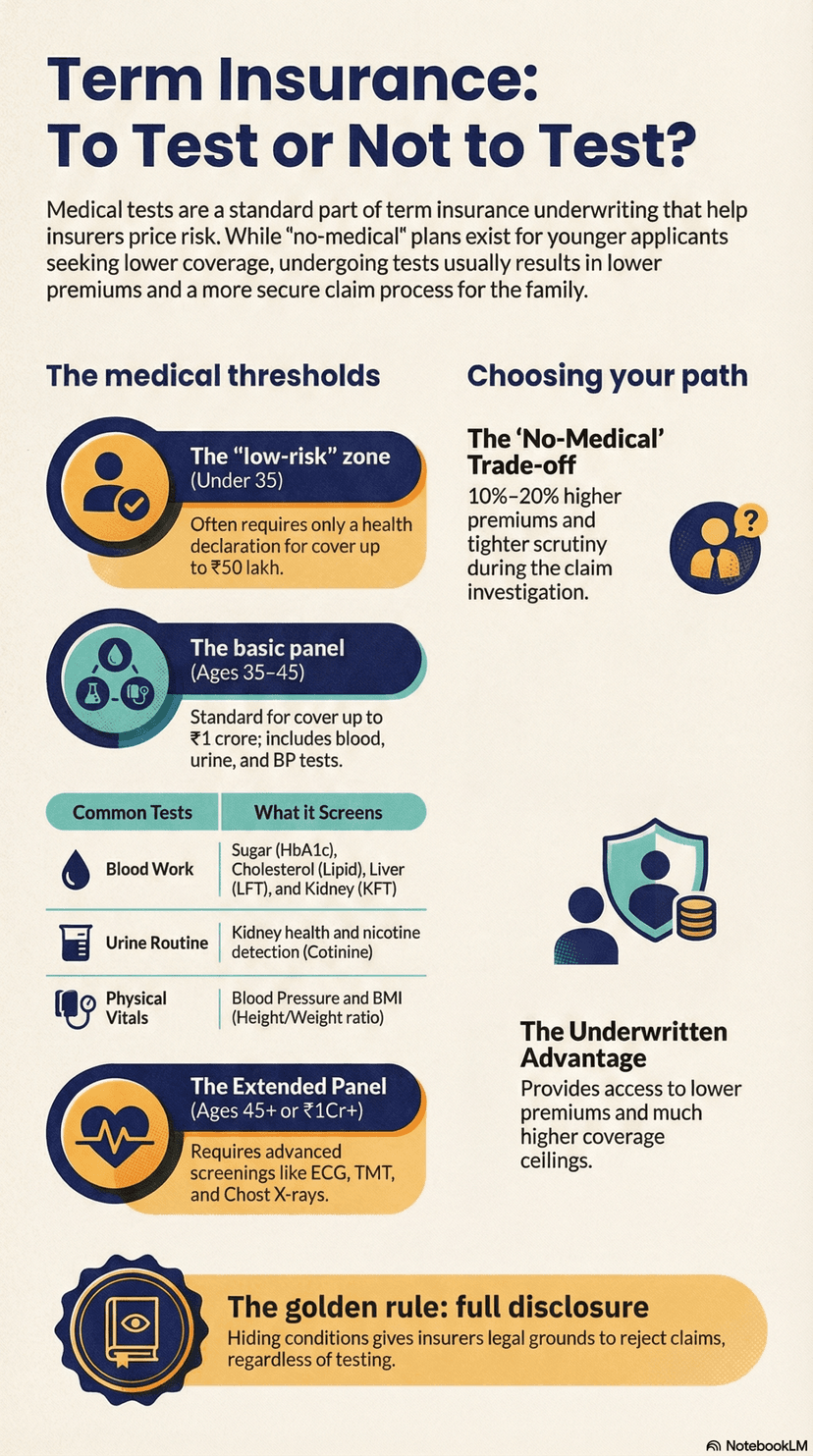

Most insurers require medical tests for term insurance if you’re over 35 or want cover above ₹50 lakh. Below those thresholds, you can often skip them.

•

Standard tests include blood work (CBC, lipid profile, sugar, liver and kidney function), urine analysis, and blood pressure. ECG, TMT, and chest X-ray kick in at higher ages or cover amounts.

•

You can buy term insurance without medical tests if you’re young (typically under 35), healthy, and willing to accept a lower cover limit (usually up to ₹50 lakh to ₹1 crore, depending on the insurer).

•

Skipping tests has trade-offs: lower cover ceilings, potentially higher premiums, and greater scrutiny at claim time.

•

Full disclosure matters regardless. Whether you take tests or not, hiding health conditions gives the insurer legal grounds to reject your family’s claim later.

Why insurers want your medical reports

A term insurance policy is a bet. You pay a small premium every year; the insurer promises to pay your family a large sum if you die during the policy term. For the insurer to price that bet accurately, they need to know how likely you are to die within the term. Your age, income, and occupation tell part of the story. Your body tells the rest.

Medical tests give the insurer a snapshot of your current health. They reveal conditions you might not even know about: early-stage diabetes, elevated cholesterol, liver enzyme irregularities, kidney function changes. Based on the results, the insurer does one of four things: accepts your application at standard rates, accepts it with a loading (higher premium), adds specific exclusions, or declines coverage altogether.

This process is called medical underwriting, and it exists to keep premiums fair for everyone in the risk pool. If insurers skipped tests entirely, healthy applicants would subsidise those with undisclosed conditions, and premiums across the board would rise.

The standard medical test panel

Every insurer has its own underwriting guidelines, but the tests fall into a predictable pattern. Here is what most insurers ask for:

Basic panel (most applicants)

| Test | What it checks |

|---|---|

| Complete Blood Count (CBC) | Red and white blood cell levels, haemoglobin, platelet count |

| Fasting Blood Sugar + HbA1c | Current blood sugar and 3-month average (diabetes screening) |

| Lipid Profile | Total cholesterol, LDL, HDL, triglycerides |

| Liver Function Test (LFT) | SGOT, SGPT, bilirubin, alkaline phosphatase |

| Kidney Function Test (KFT) | Creatinine, urea, uric acid |

| Urine Routine + Cotinine | Sugar, protein, infections; nicotine detection |

| HIV and Hepatitis B (HBsAg) | Viral screening |

| Blood Pressure | Systolic and diastolic readings |

| BMI | Height and weight ratio |

Most applicants between 35 and 45, applying for cover between ₹50 lakh and ₹1 crore, will face this panel. Younger applicants seeking lower cover may only need a subset or nothing at all.

Extended panel (higher cover or older applicants)

Once you cross 45, or your sum assured exceeds ₹1 crore to ₹2 crore, insurers typically add:

| Test | When it’s triggered |

|---|---|

| ECG (Electrocardiogram) | Age 40+ or cover above ₹1 crore |

| Treadmill Test (TMT) | Age 45+ or cover above ₹2 crore |

| Chest X-Ray | Age 45+ or tobacco users |

| Ultrasound (Abdomen) | Cover above ₹2 crore or flagged conditions |

| 2D Echocardiogram | Cover above ₹2 crore or abnormal ECG |

| Thyroid Profile | BMI outside normal range or family history |

| PSA (men 45+) | Prostate screening for older male applicants |

| Mammography (women 40+) | Breast screening for older female applicants |

Exact thresholds vary by insurer. One company might require an ECG at 40 for any cover above ₹75 lakh; another might waive it entirely for the same profile. The tables above are general patterns, not universal rules. Always confirm the specific requirements with your chosen insurer before applying.

When age and cover amount change the equation

Two variables drive how many tests you’ll face: your age and the sum assured you’re requesting.

Under 35, cover up to ₹50 lakh

You’ll often need nothing beyond a health declaration form. Insurers consider you statistically low-risk. Some may still run a random sample test or a tele-medical interview, but in many cases, you’ll get a policy issued within 24 to 48 hours with zero lab visits.

35 to 45, cover ₹50 lakh to ₹1 crore

The basic panel is standard here. Blood work, urine, BP, BMI. Some insurers add an ECG from age 40 onwards. The process takes about a week: you visit a diagnostic centre (the insurer usually arranges this at no cost to you), results go to the underwriting team, and you get a decision.

45 and above, or cover above ₹1 crore

Expect the extended panel. ECG, possibly TMT, chest X-ray, and additional screenings based on your medical history. At this age, the insurer’s risk is materially higher, and they need proportionally more data. Turnaround can stretch to two weeks depending on how quickly results come in.

If you’re a smoker or tobacco user, add cotinine testing to any tier. Tobacco use typically doubles or triples your premium, and the urine cotinine test is hard to game.

Term insurance without medical tests: how it works

Yes, you can buy term insurance without a single medical test. Several Indian insurers offer what the industry calls “simplified issue” or “no-medical” plans. But “no tests” doesn’t mean “no questions.”

Here’s what actually happens when you apply for a no-medical term plan:

- You fill out a detailed health questionnaire. This covers your medical history, current medications, chronic conditions, family health history, smoking and drinking habits, height, weight, and occupation.

- The insurer runs its own checks. They cross-reference your declarations against the Insurance Information Bureau (IIB) database, which tracks past claims, policy rejections, and medical underwriting records across the industry.

- Random sample testing is still possible. Even after waiving the medical requirement, the insurer reserves the right to call you in for a tele-medical interview or a blood test. This happens more often than applicants expect.

- The insurer decides. Based on your declarations and background checks, they accept, load, or decline.

Who qualifies for no-medical term insurance?

The typical profile:

- Age under 35 (some insurers stretch this to 45 for clean profiles)

- No pre-existing conditions: no diabetes, hypertension, heart disease, or chronic illness

- Non-smoker

- Normal BMI range

- No family history of early cardiac death or cancer

- Sum assured within the insurer’s no-medical limit (typically ₹25 lakh to ₹1 crore)

If you tick all those boxes, you can realistically expect a policy issued in one to two days, entirely online.

The cover limits

No-medical plans cap your cover at a lower amount than medically underwritten policies. The ceiling varies by insurer. Some allow up to ₹1 crore without tests for applicants under 30; others cap it at ₹25 lakh to ₹50 lakh.

If you need ₹1 crore or more in cover (and most earning members of a family do), you’ll almost certainly need to go through medical underwriting. That’s not a bad thing. Read the next section to understand why.

Why skipping tests can cost you more

No-medical policies sound convenient. No lab visit, no needles, no waiting. But the convenience comes at a price, sometimes literally.

Higher premiums

When an insurer can’t verify your health directly, they assume more risk. That risk gets passed to you as a premium loading. A 30-year-old buying ₹50 lakh cover with medical tests might pay ₹5,000 to ₹6,000 per year. The same profile without tests could pay 10% to 20% more, because the insurer is pricing in uncertainty.

Did You Know

Skipping medical tests can push annual premiums 10% to 20% higher for the same cover amount. The insurer isn’t penalising you — it’s pricing in the uncertainty of not being able to verify your health.

Lower cover ceiling

₹50 lakh to ₹1 crore might sound like a lot, but for a family with a home loan, children’s education costs, and living expenses to cover, it often falls short. Medical underwriting unlocks cover amounts of ₹2 crore, ₹3 crore, or more. If you’re the primary earner in a family, that higher ceiling matters.

Tighter claim scrutiny

This is the one that catches people off guard. When you buy a policy without medical tests, the insurer didn’t independently verify your health at the time of purchase. If a claim arises within the first few years, the investigation will be more thorough. The insurer will pull your hospital records, pharmacy purchases, pathology reports. Any condition that existed before the policy but wasn’t declared on the questionnaire could become grounds for claim rejection.

Watch Out

Without medical tests on record, a claim in the first few years triggers a thorough investigation — hospital records, pharmacy purchases, pathology reports. Any undisclosed condition can become grounds for rejection.

With a medically underwritten policy, the insurer already has your test results on file. They accepted you knowing your numbers. That makes it harder for them to deny a claim later based on a condition they could have caught during underwriting.

Pre-existing conditions: what they mean for your application

A pre-existing condition is any illness, injury, or medical status that existed before you applied for the policy. Common ones that affect term insurance underwriting in India:

- Diabetes (Type 1 or Type 2)

- Hypertension (high blood pressure)

- Heart disease (past cardiac events, stents, bypass surgery)

- Asthma or chronic respiratory conditions

- Thyroid disorders

- Obesity (BMI above 30)

- Mental health conditions (clinical depression, anxiety disorders under active treatment)

- Cancer history (even if in remission)

Having a pre-existing condition doesn’t automatically disqualify you. Insurers take one of four routes:

- Standard acceptance: Your condition is mild, well-managed, and doesn’t significantly increase mortality risk. You get standard rates.

- Acceptance with loading: Your condition raises the risk modestly. You pay a higher premium (the “loading”), typically 25% to 100% above standard rates depending on severity.

- Acceptance with exclusion: The insurer covers you but excludes death caused by the specific condition.

- Decline: The condition poses too high a risk. This is rare for well-managed conditions but does happen for recent cardiac events or active cancer.

The critical rule: disclose everything. Hiding a pre-existing condition to get a cheaper premium or avoid rejection is the single most common reason term insurance claims get rejected in India.

What happens if your application is rejected on medical grounds

A rejection stings, but it’s not permanent. Here’s how the process works and what your options are.

The rejection gets recorded

When an insurer declines your application, it gets logged in the Insurance Information Bureau (IIB) database. Other insurers can see this record when you apply elsewhere. That doesn’t mean automatic rejection from every company, but it does mean more scrutiny and questions about what happened.

You can reapply after 6 to 12 months

If the rejection was based on a manageable condition (say, high blood sugar or elevated cholesterol), most insurers allow you to reapply after six months to a year. In that window, you work on improving the specific numbers: bring your HbA1c under control, get your cholesterol down, lose weight if BMI was the issue. When you reapply, you’ll take fresh tests, and the insurer reassesses based on your new results.

Quick Tip

Use the 6 to 12 months after a rejection to actively improve the specific numbers that caused it — HbA1c, cholesterol, BMI. When you reapply, the insurer reassesses from scratch based on your fresh results.

Try a different insurer

Underwriting guidelines differ across companies. One insurer might decline you for a BMI of 33; another might accept you with a 25% loading. If you’ve been rejected, consider applying to an insurer known for flexible underwriting. Work with an advisor who understands which companies are more lenient for your specific condition.

Consider a lower cover amount

Sometimes, the rejection isn’t about your health alone but about the combination of health risk and cover amount. Requesting ₹2 crore when you’re a 45-year-old diabetic is a harder sell than requesting ₹50 lakh. Reducing the cover amount lowers the insurer’s exposure and can tip the decision in your favour.

The disclosure test: why honesty protects your family

Under IRDAI’s current framework, the Section 45 contestability period is three years from policy issuance. After three years, the insurer cannot call the policy in question on any ground whatsoever. On a plain reading of the 2015 amendment, this protection extends even to fraud, though the Supreme Court has not yet confirmed this. Before three years, any material fact you hid can become grounds for claim rejection.

Key Fact

Under IRDAI’s current framework, under Section 45 (2015 amendment), an insurer cannot call a policy in question on any ground whatsoever after three years from policy issuance. On a plain reading, this protection extends to fraud as well, though the Supreme Court has not yet confirmed this.

Here’s what “material fact” means in practice: any health condition, hospitalisation, medication, or test result that would have changed the insurer’s decision to offer you the policy or the premium they charged. A knee surgery from three years ago? Material. An episode of chest pain you got checked at a hospital? Material. The blood pressure medication your doctor prescribed last year? Material.

“But I forgot” is not a defence the insurer will accept. When your family files a claim, the investigation team will pull records from hospitals, diagnostic labs, pharmacies, and the IIB. They have both the motivation and the tools to find what you didn’t disclose.

The math is simple. A slightly higher premium (because you disclosed a condition) means your family gets paid. A cheaper premium (because you hid it) means they might get nothing. The whole point of buying term insurance for your family collapses if the claim gets rejected.

How to prepare for your term insurance medical test

If you’re going the medically underwritten route (and for most people, that’s the better choice), here’s how to make sure your tests reflect your actual health rather than a bad day:

- Fast for 10 to 12 hours before the test. Blood sugar and lipid profile results are meaningless after a meal.

- Avoid alcohol for 48 hours before. Alcohol temporarily elevates liver enzymes, which can flag your LFT results.

- Skip the gym on test day. Intense exercise can raise creatinine and white blood cell counts.

- Get a full night’s sleep. Sleep deprivation raises cortisol and blood pressure.

- Stay hydrated. Dehydration concentrates your blood and urine, which can distort readings.

- Bring a list of your medications. The diagnostic centre needs to know what you’re taking so they can interpret results correctly.

- Don’t stop prescribed medications to game the results. If you take BP or diabetes medication, keep taking it. The insurer wants to see your managed levels, not an artificially unmedicated reading that crashes once you resume the drugs.

The test itself is straightforward: a blood draw, a urine sample, blood pressure check, height and weight. If an ECG or TMT is required, it adds 30 to 45 minutes. Most insurers arrange the test at a diagnostic centre near your home or office at no cost to you.

Medical test requirements at a glance

Here’s the complete picture: what tests you’ll face based on your age and the cover amount you’re applying for.

| Your profile | Tests typically required | Expected timeline |

|---|---|---|

| Under 30, cover up to ₹50 lakh | Health declaration only; possibly tele-medical interview | 1-2 days |

| Under 35, cover ₹50 lakh-₹1 crore | Health declaration; random sample blood test possible | 2-5 days |

| 35-45, cover ₹50 lakh-₹1 crore | Full basic panel: CBC, blood sugar, HbA1c, lipid profile, LFT, KFT, urine + cotinine, HIV, HBsAg, BP, BMI | 5-7 days |

| 40-45, cover above ₹1 crore | Basic panel + ECG | 7-10 days |

| 45+, or cover above ₹2 crore | Basic panel + ECG + TMT + chest X-ray; possibly ultrasound, 2D Echo, PSA (men), mammography (women) | 10-14 days |

| Smoker or tobacco user (any age) | All tests for your age bracket + cotinine confirmation | Same as age bracket |

These are general patterns across major Indian insurers. Exact thresholds vary by company — always confirm specific requirements with your chosen insurer before applying.

Making the choice: tests or no tests?

Here’s a practical framework.

Skip the medical test if:

- You’re under 30, healthy, non-smoker, normal BMI

- You need cover of ₹50 lakh or less

- You want the policy issued fast (within a couple of days)

- You have zero pre-existing conditions and a clean family health history

- You plan to upgrade to a higher-cover, medically underwritten policy within a year or two

Take the medical test if:

- You need cover above ₹50 lakh (which most families do)

- You’re over 35

- You have any pre-existing condition, even a mild one

- You want the strongest possible claim record for your family

- You want access to lower premiums based on verified good health

For many first-time buyers in their 20s, a no-medical policy for ₹25 lakh to ₹50 lakh makes sense as a starter. It gets you covered immediately while you figure out your long-term needs. But it shouldn’t be your only policy forever. As your income grows, your liabilities increase, and your family depends on you more, upgrade to a full medically underwritten policy with adequate cover.

FAQs

Can I get term insurance without a medical test?

Yes. Several Indian insurers offer term plans without medical tests, typically for applicants under 35 to 45 years old with no pre-existing conditions and a sum assured up to ₹50 lakh to ₹1 crore. You’ll still need to fill out a health declaration, and the insurer may run background checks or request a random tele-medical interview.

What medical tests are required for term insurance?

The standard panel includes a Complete Blood Count, fasting blood sugar, HbA1c, lipid profile, liver function test, kidney function test, urine analysis with cotinine screening, HIV and Hepatitis B tests, blood pressure, and BMI measurement. Applicants over 40 or seeking cover above ₹1 crore may also need an ECG, treadmill test, chest X-ray, or ultrasound.

Is term insurance without medical tests more expensive?

Usually, yes. Insurers charge a risk premium when they can’t verify your health through tests. Expect 10% to 20% higher premiums compared to a medically underwritten policy for the same age and cover amount. The gap narrows for very young, healthy applicants.

What qualifies as a pre-existing condition for term insurance?

Any illness, injury, or medical condition diagnosed before you apply. Common ones include diabetes, hypertension, heart disease, asthma, thyroid disorders, obesity, mental health conditions under treatment, and cancer (including remission). Disclose all of them; non-disclosure can lead to claim rejection.

Can I reapply if my term insurance application is rejected on medical grounds?

Yes. Most insurers allow reapplication after 6 to 12 months. Use that time to improve the health metrics that caused the rejection (blood sugar, cholesterol, BMI). You can also apply to a different insurer, as underwriting standards vary. Consider a lower cover amount if your health profile and the requested sum assured together exceeded the insurer’s risk appetite.

What is the moratorium period for non-disclosure in term insurance?

Under current IRDAI guidelines, the Section 45 contestability period is three years from policy issuance. After three years, the insurer cannot call the policy in question on any ground whatsoever. On a plain reading of the 2015 amendment, even fraud challenges are limited to within 3 years, though the Supreme Court has not yet confirmed this. Before three years, any undisclosed material fact can be used to deny a claim.

Related Reading

Try our free tools

Disclaimer: This article is for informational purposes only and does not constitute insurance advice. Consult an IRDAI-registered insurance advisor for recommendations tailored to your specific financial situation and needs.

Was this article helpful?

Your feedback helps us improve our guides

Reviewed and Edited by

Ashok HegdeAshok Hegde is the Chief Executive Officer at Quantent, where he leads a team of media professionals helping clients leverage digital media for better business outcomes. With over 30 years of experience across print and digital media, he advises clients on content and media strategy — from startups to established brands. His focus is on helping organisations use online media — social, search, and mobile — to build brand awareness, drive sales, and protect reputation.