Why Your Agent Doesn’t Recommend Term Insurance: IRDAI’s Commission Probe

Updated 5 min read

IRDAI has quietly begun asking every life insurer in the country to hand over granular data on how commissions flow through the system, Moneycontrol reported on April 15. The regulator wants channel-wise payouts (agency, bancassurance, brokers, direct), product-level splits (ULIP, participating, non-participating), first-year versus renewal breakdowns, and distributor-level earnings including bonuses, non-cash rewards, and persistency metrics.

This is not a routine data call. ICICI Prudential Life’s CFO Dhiren Salian confirmed to Moneycontrol that the regulator has sought “granular, bottom-up data on commission structures,” though no formal proposal has been circulated yet. The level of detail points to a diagnostic exercise, with IRDAI attempting to map where incentives flow and where distortions are emerging.

The commission gap at a glance: In FY25, life insurers paid around ₹60,800 crore in commissions, up 18% year on year, while premium growth came in at just 6.7%. The commission expense ratio climbed to 6.86% from 6.21%. Distribution costs are growing nearly three times faster than the business itself.

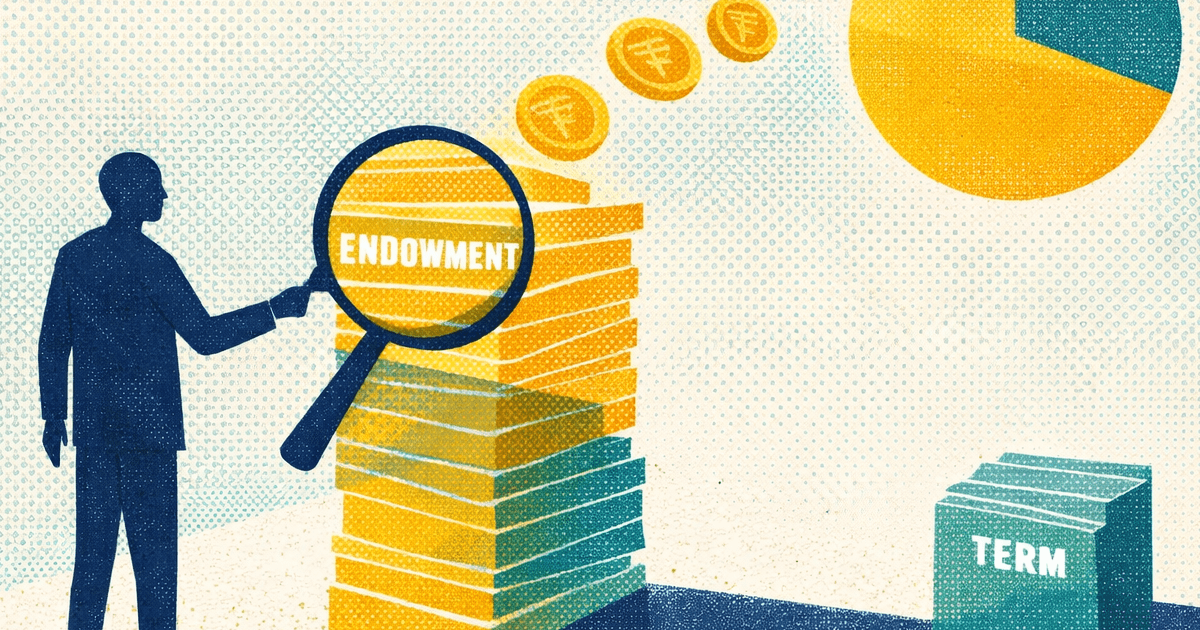

If you have ever wondered why your insurance agent pitched you an endowment plan or a ULIP instead of a term policy, the commission structure is the short answer.

A ₹1 crore term plan for a healthy 35-year-old costs roughly ₹12,000 a year. The agent’s first-year commission on that? A few hundred rupees. An endowment policy with ₹50,000 in annual premium can yield the agent several thousand rupees in year one, plus renewal income for 15-20 years. The math makes the sales conversation predictable.

This is not speculation. A February 2026 survey of 450 insurance buyers and 300 agents across 20 Indian cities (published by Upstox and Fingrowth Media) found that 83% of agents earned over 10% commission on first-year premiums. Nearly half (48%) reported that contest-driven incentives steered them towards high-commission products. And 39% admitted to commission pass-backs as rebates, a practice that is illegal under IRDAI regulations.

From the buyer’s side: 63% of respondents said they believed their agent had prioritised personal commissions over the buyer’s needs. 47% said actual returns fell below expectations. And 39% felt misled or under-informed at the time of purchase. 93% of respondents in the survey owned endowment or ULIP products.

IRDAI has been moving in this direction for a while. In April 2023, it abolished product-specific commission caps and left each insurer free to set its own schedule, subject to an overall expense ceiling at the company level. Endowment commissions stayed high; term commissions stayed low.

Parliament’s passage of the Insurance Amendment Act in December 2025 gave IRDAI explicit new powers to regulate commission structures. The data-gathering exercise reported by Moneycontrol suggests the regulator is now building the evidence base to act on those powers.

The question is whether any restructuring will narrow the commission gap between term and traditional products enough to change agent behaviour. If selling a term plan and selling an endowment become roughly equivalent in earnings-per-hour for the agent, the sales conversation changes. If the gap stays wide, agents will continue to do what any rational economic actor would do: sell the product that pays them more.

Watch for the draft norms. IRDAI is expected to publish draft commission regulations in the coming months, potentially modelled on SEBI’s approach to mutual fund commissions. The final framework could take a year or longer to implement.

Compare online. Aggregator platforms already let you compare term plans across insurers without an agent in the loop. The premium you see is the premium you pay.

Ask your agent one question. If someone recommends a savings-linked insurance product, ask them to write down the projected internal rate of return at maturity. The survey found that 60% of agents did not fully understand IRR themselves, and only 17% consistently explained it to buyers. If the agent cannot answer, that tells you what you need to know about the advice you are getting.

Check your existing cover. If your only life insurance is an endowment or money-back plan, the sum assured is likely a fraction of what your family would need. A separate term policy fills that gap at a fraction of the cost. Our guide on spotting mis-selling warning signs can help you evaluate whether your current policies were the right fit.

Channel-wise commission payouts (agency, bancassurance, brokers, direct), product-level commission structures (ULIP, participating, non-participating), first-year versus renewal splits, distributor-level earnings including bonuses and non-cash rewards, expense of management ratios, and persistency metrics.

Term insurance commissions are already low, so any restructuring is unlikely to change term premiums significantly. The bigger impact would be on endowment and ULIP commissions, which could narrow the gap that currently incentivises agents to sell savings products over protection products.

No. Draft commission norms have not been published yet, and the final framework could take a year or more to implement. Term insurance premiums are based on your age at the time of purchase. Waiting makes the policy more expensive regardless of commission changes.

Sources: Moneycontrol (Apr 15, 2026); Upstox/Fingrowth Media, “India’s One-Hour Insurance Problem” survey (Feb 2026); CafeMutual on Insurance Amendment Act 2025.

Disclaimer: This article is for informational purposes only and does not constitute insurance advice. Consult an IRDAI-registered insurance advisor for recommendations tailored to your specific financial situation and needs.

Was this article helpful?

Your feedback helps us improve our guides

Reviewed and Edited by

Gyansurance EditorialThe Gyansurance Editorial team is a mix of financial journalists, insurance advisors and copy editors. Together, we are aiming to demystify life insurance for Indian readers around the world.

IRDAI has asked insurers to define “claim” and standardise claim settlement ratio. The answer matters for every term insurance buyer comparing CSRs.

100% FDI, Bima Trinity, zero GST, and a distribution reform crackdown. Every 2026 insurance reform explained with what it means for you.

NHRC issued a notice to IRDAI after disabled persons were denied life insurance. The legal framework, IRDAI guidelines, and your rights as a buyer explained.